On 19 April 2024, HKEX published an announcement titled “Exchange Publishes Conclusions on Climate Disclosure Requirements” (http://www.hkex.com.hk/news/regulatory-announcements/2024/240419news?sc_lang=en), informing about the New Climate Requirements that will align more closely with IFRS S2. These requirements will be effective from 1 January 2025 and will be implemented in phases. Here, we summarize the major changes and important points:

| Disclosure of scope 1 and scope 2 GHG emissions | Disclosures other than scope 1 and scope 2 GHG emissions | |

| Large Cap Issuers |

Mandatory disclosure (Financial years commencing on or after 1 January 2025) |

“Comply or explain”: in financial years commencing on or after 1 January 2025 Mandatory disclosure: in financial years commencing on or after 1 January 2026 |

| Main Board Issuers (other than Large Cap Issuers) | Mandatory disclosure (Financial years commencing on or after 1 January 2025) |

“Comply or explain” (Financial years commencing on or after 1 January 2025) |

| GEM issuers | Mandatory disclosure (Financial years commencing on or after 1 January 2025) |

Voluntary disclosure (Financial years commencing on or after 1 January 2025) |

The new requirements have been updated from Appendix C2 ESG Reporting Guide to Appendix C2 ESG Reporting Code.

Additionally, KPI A1.2 & KPI A4 of the current Guide have been expanded and now form a new part, Part D Climate-related Disclosure, in the New Code.

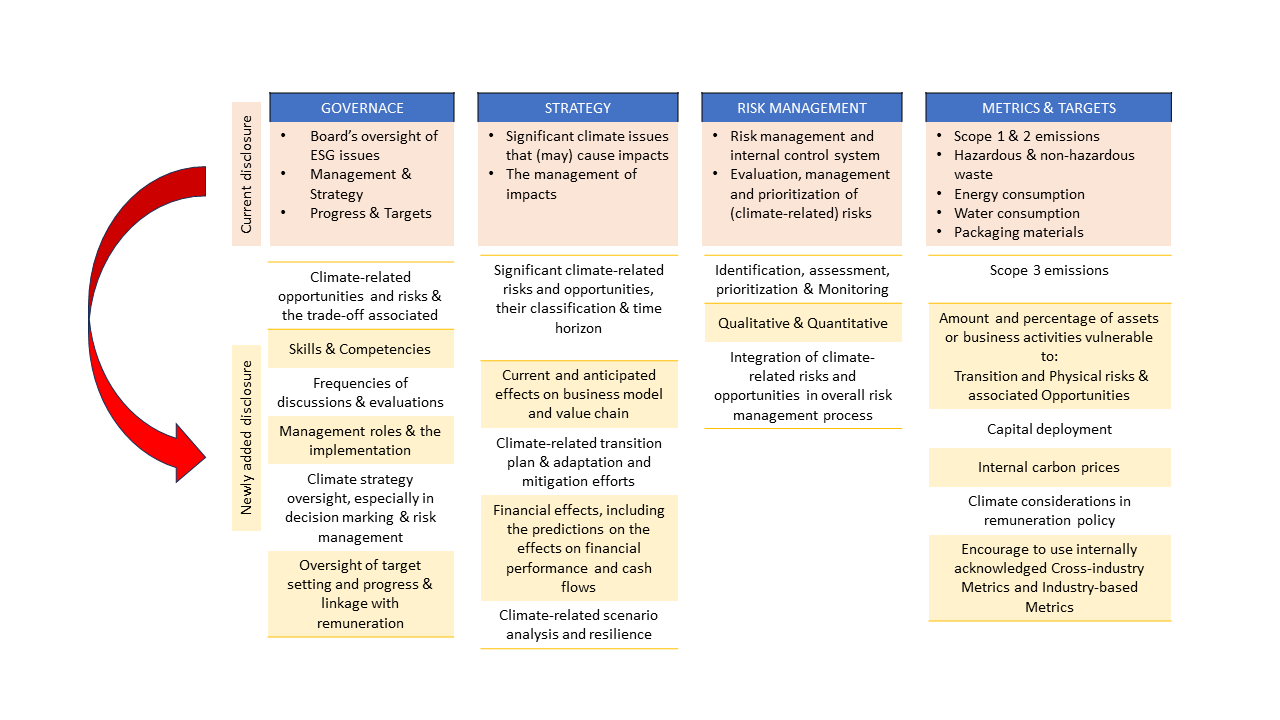

The key points of Part D of ESG Reporting Code are as follows:

To get prepared for the updates, please feel free to contact us at 852-3702 3030 or info@pro-wis.com.hk.

For more details, please refer to the announcement, as well as the Consultation Conclusion and Implementation Guidance published by the HKEx.

2024© PRO-WIS Risk Advisory Services Limited. All rights reserved